Calculate Your Loan Repayment Instantly

This introduction will discuss the essential elements of comprehending Malaysian home loans and the current trends affecting the local housing loan Malaysia market in 2023.

Understanding Housing Loan Malaysia

Many Malaysians use housing loans to finance their investment when buying a home. A housing loan, usually a home loan or mortgage, is a financial product that banks and other financial organisations provide to help people purchase homes. These loans give borrowers the money they need to buy the homes they want and offer adjustable repayment periods to fit their budgets.

Borrowers in Malaysia often need to meet certain eligibility requirements to obtain a housing loan. These requirements might include being employed, having a steady income, and satisfying the minimum age and credit requirements imposed by the lenders. The housing loan Malaysia amount granted is determined by several variables, including the borrower’s income, creditworthiness, and property valuation. Borrowers must also consider other important factors, including the housing loan length, housing loan interest rates, and associated costs.

Recent Trends in Malaysia’s Housing Loan Market

Several notable trends in housing loan Malaysia sector in 2023 have influenced how prospective homeowners can borrow money. The availability of low-interest housing loans is one noticeable development. Financial institutions have created competitive low-interest housing loans to entice borrowers as the demand for affordable housing keeps rising. People now have more opportunities to obtain house loans with advantageous terms, allowing them to manage their money better.

Further development in Malaysia’s housing loan Malaysia sector is a stronger focus on digital accessibility and convenience. The procedure of applying for a loan has been simplified thanks to the development of online and mobile platforms by banks and other financial organisations. Borrowers can readily access house loan calculator through various digital channels, compare housing loan Malaysia interest rates, and submit their applications comfortably from the convenience of their homes.

Furthermore, Malaysian homeowners are becoming increasingly familiar with the idea of refinancing. Borrowers can refinance their old mortgages to replace them with new ones with better interest rates and repayment terms. This pattern has allowed borrowers to lighten their financial load and exploit opportune market circumstances to maximise their loan commitments.

What you should know about home loans in Malaysia

Due to the numerous terms you’d need to be aware of, and the processes it takes from making an offer to purchasing up to receiving the keys in your hands, buying and owning a home is typically difficult and occasionally daunting for first-time home purchasers.

Therefore, here are a few things to know to help you better grasp this procedure before applying for a mortgage.

Types of Housing Loan Malaysia

Understanding the many housing loan Malaysia options available to consumers is crucial when considering a home loan in Malaysia. Here are the three most typical forms of mortgages in Malaysia:

- Term Loan: The most fundamental kind of mortgage is a term loan. It has a set repayment schedule, with a regular monthly payment over the course of the loan. Those who like predictable monthly instalments should choose this form of credit.

- Semi-Flexi Loan: Borrowers have some flexibility with semi-flexi loans. It enables you to make additional payments to lower the loan principal and interest payments. The increased payments, however, cannot be withdrawn. This loan is excellent for people wanting to speed up repayment while retaining flexibility.

- Flexi Loan: Borrowers have the most freedom with flex loans. You can use it to reduce the loan principal and interest payments by depositing extra money into a linked current account. Additionally, you can withdraw extra money as needed. Individuals with variable income or occasionally needing additional funds might benefit from this loan.

Understanding the different types of housing loan Malaysia will help you choose the one that aligns with your financial goals and preferences.

Factors to Consider When Choosing a Housing Loan

To choose a housing loan Malaysia wisely, it is important to consider the following factors:

- Interest Rates: Interest rates from various banks and financial institutions should be compared. Over the course of the loan, a low-interest housing loans can result in significant financial savings for you. Consider whether you want a set or variable interest rate that changes depending on the market.

- Loan Tenure: It is important to compare low-interest housing loans offered by different banks and financial institutions. A reduced housing loan interest rate can help you save a lot of money over the course of the loan. Consider whether you want a fixed interest rate or one fluctuating in response to the market.

- Repayment Flexibility: It’s crucial to compare the low-interest housing loans that various banks and financial organisations provide. You can save a lot of money over the course of low-interest housing loans. Consider whether you want a set interest rate or one that varies depending on the market.

- Fees and Charges: It’s critical to compare the low-interest housing loans offered by different banks and financial institutions. With low-interest housing loans, you can save a lot of money over the life of the housing loan Malaysia. Consider whether you want a fixed interest rate or one that changes with the market.

Considering these aspects, you can choose a house loan that best meets your financial needs and long-term goals.

Detailed Review of Top Housing Loan Providers in Malaysia

1. Bank Negara Malaysia: The Premier Choice

One of the nation’s top lenders of housing loans in Malaysia is usually regarded as Bank Negara Malaysia. Bank Negara Malaysia provides various housing loan Malaysia solutions designed to fulfil the various demands of Malaysian borrowers as part of its commitment to fostering homeownership and guaranteeing financial stability.

Types of Housing Loans Offered

To meet varied needs, Bank Negara Malaysia offers several different forms of home loans:

- Term Loan: Bank Negara Malaysia offers term loans with predetermined repayment terms and fixed monthly instalments. This loan is appropriate for borrowers who like steady and regular repayments.

- Flexi Loan: A flex loan allows borrowers to make additional payments to lower the loan principal and cut interest costs. The extra payments can be stopped if necessary, giving the loan manager more flexibility.

Interest Rates & Payment Terms

Bank Negara Malaysia offers competitive low-interest housing loans based on factors such as the Base Rate (BR) and the borrower’s creditworthiness. Let’s consider an example to understand the payment terms:

- Example:

- Loan Amount: RM500,000

- Loan Tenure: 30 years (360 months)

- Interest Rate: 3.50% per annum

Using these parameters, we can calculate the monthly installment and total repayment amount:

Monthly Installment Calculation:

- Monthly Interest Rate = Annual Interest Rate / 12 months

Monthly Interest Rate = 3.50% / 12 = 0.29% - Monthly Installment = (Loan Amount * Monthly Interest Rate) / (1 – (1 + Monthly Interest Rate)^(-Loan Tenure))

Monthly Installment = (500,000 * 0.29%) / (1 – (1 + 0.29%)^(-360))

Total Repayment Calculation:

- Total Repayment = Monthly Installment * Loan Tenure

Please note that this is just an illustration, and the actual housing loan Malaysia interest rates and payment terms may vary based on individual circumstances and housing oan eligibility.

Customer Service Evaluation

Customer service at Bank Negara Malaysia is renowned for being top-notch. By offering prompt and accurate support throughout the housing loan application process, the bank puts the needs of its clients first. Their committed customer service team ensures borrowers receive thorough instruction and support, immediately responding to questions or issues.

To efficiently manage their housing loan accounts, track repayments, and obtain crucial loan-related information, borrowers can visit online portals or mobile applications supplied by Bank Negara Malaysia.

The dedication of Bank Negara Malaysia to providing exceptional customer service distinguishes them as a leading provider of housing loan Malaysia.

2. CIMB Group: A Comprehensive Banking Solution

Leading Malaysian financial company CIMB Group provides various financial services and products, including mortgage loans. The CIMB Group has made a name for itself as a top option for consumers looking for housing financing solutions because of its dedication to client satisfaction and competitive housing loan Malaysia offerings.

Types of Housing Loans Offered

To meet the diverse needs and preferences of Malaysian borrowers, CIMB Group offers a range of housing loan Malaysia:

- Term Loan: CIMB offers term loans with predetermined repayment terms and fixed monthly instalments. The repayment plan for this kind of loan is predictable and stable for the borrower.

- Flexi Loan: Term loans with fixed monthly payments and predetermined repayment terms are available from CIMB. This type of loan has a predictable and stable payback schedule for the borrower.

Interest Rates & Payment Terms

To illustrate the payment terms, let’s consider an example:

- Example:

- Loan Amount: RM500,000

- Loan Tenure: 20 years (240 months)

- Interest Rate: 4.00% per annum

Using these parameters, we can calculate the monthly installment and total repayment amount:

Monthly Installment Calculation:

- Monthly Interest Rate = Annual Interest Rate / 12 months

Monthly Interest Rate = 4.00% / 12 = 0.33% - Monthly Installment = (Loan Amount * Monthly Interest Rate) / (1 – (1 + Monthly Interest Rate)^(-Loan Tenure))

Monthly Installment = (500,000 * 0.33%) / (1 – (1 + 0.33%)^(-240))

Total Repayment Calculation:

Total Repayment = Monthly Installment * Loan Tenure

Please note that this is just an illustration, and the actual housing loan Malaysia interest rates and payment terms may vary based on individual circumstances and loan eligibility.

Customer Service Evaluation

The CIMB Group places a high value on providing excellent customer service. They make an effort to make the entire loan application process—and beyond—for borrowers seamless and trouble-free. The CIMB Group ensures that borrowers receive timely and dependable assistance, answering any questions or issues by dedicating teams to customer service.

Additionally, borrowers have access to CIMB Group’s mobile applications and online banking platforms, making it simple to manage their loan accounts, keep payments, and obtain vital loan-related data.

The CIMB Group is a dependable and trustworthy option for house loans in Malaysia due to its dedication to providing exceptional customer care.

3. Maybank: Traditional yet Reliable

In Malaysia, Maybank is a reputable and well-established banking company that provides various financial services and products, including mortgage loans. Maybank Malaysia has established a solid reputation as a reliable option for borrowers looking for house financing solutions because of its extensive presence and dedication to customer satisfaction.

Types of Housing Loans Offered

To meet the wide range of demands and preferences of Malaysian borrowers, Maybank offers several housing loan Malaysia options:

- Term Loan: Maybank offers term loans with predetermined repayment terms and fixed monthly payments. The repayment plan for this kind of loan is predictable and stable for the borrower.

- Flexi Loan: With Maybank’s flexible loan option, borrowers can make extra payments to lower their loan principal and interest costs. Greater control over loan management is made possible by the freedom to deposit additional money and remove them as necessary.

Interest Rates & Payment Terms

To illustrate the payment terms, let’s consider an example:

- Example:

- Loan Amount: RM500,000

- Loan Tenure: 30 years (360 months)

- Interest Rate: 3.50% per annum

Using these parameters, we can calculate the monthly installment and total repayment amount:

Monthly Installment Calculation:

Monthly Interest Rate = Annual Interest Rate / 12 months

Monthly Interest Rate = 3.50% / 12 = 0.29%

Monthly Installment = (Loan Amount * Monthly Interest Rate) / (1 – (1 + Monthly Interest Rate)^(-Loan Tenure))

Monthly Installment = (500,000 * 0.29%) / (1 – (1 + 0.29%)^(-360))

Total Repayment Calculation:

Total Repayment = Monthly Installment * Loan Tenure

Please note that this is just an illustration, and the actual housing loan Malaysia interest rates and payment terms may vary based on individual circumstances and loan eligibility.

Customer Service Evaluation

Maybank places a high priority on providing superior customer service. The bank makes every effort to make the housing loan application procedure seamless and customer-focused. By employing a devoted customer care team, Maybank ensures that borrowers receive timely and dependable assistance for any questions or problems.

Additionally, Maybank offers user-friendly mobile applications and internet platforms for borrowers, making it simple to manage their housing loan accounts, keep track of their repayments, and access vital housing loan-related data.

Due to its history of dependability and dedication to client satisfaction, Maybank is regarded as a reliable and trustworthy option for housing loan Malaysia.

3. Public Bank Berhad: Customer-Centric Approach

A well-known banking organisation in Malaysia, Public Bank Berhad is noted for its customer-centric philosophy and a wide array of financial products and services. Public Bank Berhad provides affordable options for house loans to satisfy the various requirements and tastes of Malaysian borrowers.

Types of Housing Loans Offered

Public Bank Berhad offers different housing loan Malaysia solutions to meet different needs:

- Conventional Term Loan: Traditional term loans from Public Bank Berhad have fixed monthly payments for a set period of time. The repayment schedule for this form of loan is stable and predictable.

- Flexi Loan: The flexi loan option from Public Bank Berhad enables borrowers to make additional payments to lower the loan principal and cut interest costs. Borrowers can more effectively manage their loans by depositing more funds and withdrawing them as needed.

Interest Rates & Payment Terms

Interest Rates:

- The housing loan Malaysia interest rates offered by Public Bank Berhad for housing loans are competitive and vary based on factors such as the loan amount, financing tenure, and the borrower’s creditworthiness.

- As an example, let’s consider a housing loan with a loan amount of RM500,000 and a financing tenure of 30 years.

- The housing loan interest rate for this housing loan may be 3.5% per annum.

Payment Terms:

- Public Bank Berhad provides flexible repayment tenures to suit borrowers’ needs. In this example, let’s assume a financing tenure of 30 years.

- Based on the loan amount of RM500,000 and an interest rate of 3.5% per annum, the monthly installment for this loan can be calculated using a housing loan calculator.

- The monthly installment for this loan may amount to approximately RM2,245.

Early Settlement and Partial Prepayment:

- Public Bank Berhad may offer options for early settlement or partial prepayment of the housing loan.

- For example, borrowers can make extra payments towards the principal amount to reduce the outstanding housing loan balance.

- Early settlement and partial prepayment options can help borrowers save on overall interest costs and potentially shorten the repayment period.

Customer Service Evaluation

An essential focus for Public Bank Berhad is delivering top-notch customer service. Throughout the application process for a housing loan, the bank aims to provide a seamless and tailored experience. Public Bank Berhad ensures borrowers receive timely advice and direction, addressing any questions or problems, thanks to a devoted customer care team.

Additionally, Public Bank Berhad provides user-friendly mobile and web platforms that make it simple to manage housing loan accounts, access vital housing loan-related data, and contact the bank’s customer support staff.

Public Bank Berhad is a dependable and reputable option for housing loan Malaysia thanks to its customer-centric philosophy and dedication to service quality.

4. RHB Bank: Tailoring Your Home Loan Needs

Leading Malaysian bank RHB Bank is renowned for its dedication to creating housing loan Malaysia solutions tailored to each borrower’s requirements. RHB Bank has a significant presence in the housing loan Malaysia market and provides a wide range of goods and services to help Malaysians realise their dream of home ownership.

Types of Housing Loans Offered

RHB Bank offers the following housing loan options to meet the various needs of borrowers:

- Conventional Home Loans: Traditional home loans from RHB Bank are available with fixed or variable housing loan interest rates. Borrowers can select one of these options depending on their preferences and level of risk tolerance. While variable housing loan Malaysia interest rates allow borrowers to possibly profit from market changes, fixed interest rates offer stability.

- Islamic Home Financing: RHB Bank provides Shariah-compliant home finance options for clients seeking Islamic banking. These financing choices follow Islamic principles and offer features and advantages to satisfy Muslim borrowers’ requirements.

Interest Rates & Payment Terms

Interest Rates:

- RHB Bank offers competitive interest rates for housing loan Malaysia. The housing loan interest rate may vary depending on the loan amount, financing tenure, and the borrower’s creditworthiness.

- As an example, let’s consider a housing loan with a loan amount of RM400,000 and a financing tenure of 20 years.

- The housing loan interest rate for this loan maybe 3.8% per annum.

Payment Terms:

- RHB Bank provides flexible repayment options to accommodate borrowers’ financial capabilities. In this example, let’s assume a financing tenure of 20 years.

- Based on the housing loan amount of RM400,000 and an interest rate of 3.8% per annum, the monthly installment for this loan can be calculated using a housing loan calculator.

- The monthly installment for this housing loan may amount to approximately RM2,449.

Early Settlement and Partial Prepayment:

- RHB Bank may offer options for early settlement or partial prepayment of the housing loan.

- Borrowers have the flexibility to make extra payments towards the principal amount, which can help reduce the outstanding housing loan balance and potentially save on overall interest costs.

- Early settlement and partial prepayment options allow borrowers to repay their housing loan sooner and achieve financial freedom.

Customer Service Evaluation

Throughout the whole home loan process, RHB Bank prioritises customer happiness and works to provide superior customer service. The committed team of specialists at the bank offers specialised support and direction, ensuring that borrowers know the housing loan application procedure and their lending possibilities.

In-branch assistance, phone helplines, and internet platforms are just a few simple ways RHB Bank provides client support. These systems make it possible for borrowers to obtain information, monitor the status of their loan applications, and get help right away when they need it.

With its customer-centric approach and commitment to meeting individual needs, RHB Bank stands out as a trusted partner in the housing loan in Malaysia market.

5. Bank of China Malaysia Home Loan

A well-known financial institution, Bank of China Malaysia, provides a variety of banking goods and services, including mortgage loans. Bank of China Malaysia offers competitive housing loan Malaysia alternatives to fulfil the varied demands of Malaysian borrowers thanks to its significant experience in the banking sector and global presence.

Types of Housing Loans Offered

Bank of China Malaysia offers the following types of housing loans:

- Home Loan: The Bank of China Home Loan is intended to support people and families in realising their dream of home ownership. This lending option offers funding for both finished and under-construction properties. Depending on their preferences and financial capabilities, flexible repayment terms are available for borrowers to select from.

- Refinancing Loan: Borrowers who want to refinance their existing housing loans from other banks can do so through the Bank of China Malaysia. Borrowers may benefit from significant interest savings and improved loan conditions thanks to the refinancing loan, which can help them better manage their money.

Interest Rates & Payment Terms

Interest Rates:

- Bank of China Malaysia offers competitive housing loan interest rates for housing loans. The housing loan interest rate may vary depending on the housing loan amount, financing tenure, and the borrower’s creditworthiness.

- As an example, let’s consider a housing loan with a loan amount of RM500,000 and a financing tenure of 25 years.

- The housing loan interest rate for this housing loan maybe 4.5% per annum.

Payment Terms:

- Bank of China Malaysia provides flexible repayment options for borrowers’ financial needs. In this example, let’s assume a financing tenure of 25 years.

- Based on the loan amount of RM500,000 and an interest rate of 4.5% per annum, the monthly installment for this housing loan can be calculated using a house loan calculator.

- The monthly installment for this housing loan may amount to approximately RM2,936.

Early Settlement and Partial Prepayment:

- Bank of China Malaysia may offer options for early settlement or partial prepayment of the housing loan.

- Borrowers have the flexibility to make additional payments towards the principal amount, which can help reduce the outstanding housing loan balance and potentially save on overall interest costs.

- Early settlement and partial prepayment options allow borrowers to pay off their housing loan faster and potentially save on interest charges.

Customer Service Evaluation

Throughout the home loan application process, the Bank of China Malaysia prioritises customer happiness and works to provide superior customer service. The bank’s committed team of specialists is committed to offering borrowers customised support and guidance, ensuring a simple and straightforward process.

Customers may get full support Through various channels, including in-branch consultations, phone helplines, and online platforms. Inquiries and complaints from customers are valued by Bank of China Malaysia, which strives to respond to them quickly and effectively.

The bank’s customer-centric strategy goes beyond the application process; borrowers are kept in constant communication with and supported throughout the life of the housing loan. The Bank of China Malaysia aims to develop lasting connections with its clients by consistently offering dependable and effective service.

6. Alliance Islamic Bank

Alliance Islamic Bank is Malaysia’s leading financial institution focusing on Islamic banking solutions. Alliance Islamic Bank is strongly committed to providing Shariah-compliant goods and services, and it provides a selection of housing loan choices made to satisfy the various requirements of Malaysian homebuyers.

Types of Housing Loans Offered

Alliance Islamic Bank offers the following residential loan products:

- Home Financing-i: This is a flexible and cost-effective financing option based on the Musharakah Mutanaqisah principle. Home Financing-i provides solutions for completed and under-construction properties, competitive profit rates, and flexible financing terms. This financing option allows Customers to take advantage of homeownership benefits while adhering to Islamic values.

- i-Wish Home Financing-i: I-Wish Home Financing-i offers a customisable profit rate structure that adapts based on current market rates and is made for customers looking for a special financing option. Customers can pay more to shorten the financing term with low-interest housing loans.

Interest Rates & Payment Terms

Interest Rates:

- Alliance Islamic Bank offers competitive housing loan interest rates for its housing loans. The housing loan interest rate may vary depending on the housing loan amount, financing tenure, and the borrower’s creditworthiness.

- As an example, let’s consider a housing loan with a loan amount of RM500,000 and a financing tenure of 30 years.

- The housing loan interest rate for this loan maybe 4.25% per annum.

Payment Terms:

- Alliance Islamic Bank provides flexible repayment options to accommodate borrowers’ financial capabilities. In this example, let’s assume a financing tenure of 30 years.

- Based on the loan amount of RM500,000 and an interest rate of 4.25% per annum, the monthly installment for this housing loan can be calculated using a house loan calculator.

- The monthly installment for this housing loan may amount to approximately RM2,458.

Early Settlement and Partial Prepayment:

- Alliance Islamic Bank may offer options for early settlement or partial prepayment of the housing loan.

- Borrowers have the flexibility to make additional payments towards the principal amount, which can help reduce the outstanding housing loan balance and potentially save on overall interest costs.

- Early settlement and partial prepayment options allow borrowers to pay off their housing loan faster and potentially save on interest charges.

Customer Service Evaluation

To give its clients a seamless borrowing experience, Alliance Islamic Bank is committed to providing great customer service. The bank focuses on developing enduring relationships with its clients and provides individualised support throughout the housing loan application process.

Customers can access comprehensive support through various channels, including in-person meetings, toll-free hotlines, and online resources. The experienced and helpful employees at Alliance Islamic Bank are available to respond to customer questions, offer advice, and help with any issues relating to home loans.

The bank’s proactive approach to resolving problems and guaranteeing prompt responses to consumer inquiries demonstrate its dedication to ensuring customer happiness. Customers can count on Alliance Islamic Bank to provide dependable and effective service throughout the housing financing process.

7. AIA Home Loan

AIA, A reputable insurance brand, provides complete financial solutions like mortgage loans. The AIA Home Loan was created to offer Malaysians adaptable and cost-effective financing solutions for their ideal homes.

Types of Housing Loans Offered

A selection of housing loan Malaysia options from AIA is available to accommodate various requirements and tastes:

- Conventional Home Loans: The conventional home loan from AIA is a simple financing choice with reasonable housing loan interest rates. It gives borrowers the money to buy or refinance residential real estate. Borrowers can select from various housing loan terms to suit their financial situation best.

- Islamic Home Financing: The Islamic Home Loan from AIA adheres to the rules of finance that comply with Shariah. It provides flexible funding solutions that are open and equitable. By adhering to the Tawarruq principle, the Islamic Home Loan enables borrowers to take advantage of homeownership while adhering to Islamic financial norms.

Interest Rates & Payment Terms

Interest Rates:

- AIA Home Loan offers competitive housing loan interest rates for its housing loans. The housing loan interest rate may vary depending on the housing loan amount, financing tenure, and the borrower’s creditworthiness.

- As an example, let’s consider a housing loan with a loan amount of RM400,000 and a financing tenure of 20 years.

- The housing loan interest rate for this loan maybe 4.50% per annum.

Payment Terms:

- AIA Home Loan provides flexible repayment options to suit borrowers’ financial needs. In this example, let’s assume a financing tenure of 20 years.

- Based on the housing loan amount of RM400,000 and an interest rate of 4.50% per annum, the monthly installment for this housing loan can be calculated using a house loan calculator.

- The monthly installment for this housing loan may amount to approximately RM2,519.

Early Settlement and Partial Prepayment:

- AIA Home Loan may offer options for early settlement or partial prepayment of the housing loan.

- Borrowers have the flexibility to make additional payments towards the principal amount, which can help reduce the outstanding housing loan balance and potentially save on overall interest costs.

- Early settlement and partial prepayment options allow borrowers to pay off their housing loan faster and potentially save on interest charges.

Customer Service Evaluation

For its clients, AIA is dedicated to providing first-rate customer service and a hassle-free borrowing experience. The business has a committed staff of experts who offer individualised support and direction throughout the housing loan application procedure. They work hard to respond to consumer questions quickly and offer accurate information so borrowers can make wise selections.

AIA provides various customer assistance options, such as in-person meetings, phone hotlines, and online forums. Through these channels, borrowers can get the information they require, follow the progress of their housing loan applications, and get rapid assistance if they do.

AIA is a dependable option for Malaysians looking for house loan solutions thanks to its reputable brand and customer-centric philosophy.

8. UOB Home Loan

The leading financial organisation in Malaysia, UOB (United Overseas Bank) provides a wide range of banking services, including mortgage loans. In addition to offering reasonable housing loan interest rates and flexible lending terms, UOB is renowned for its dedication to customer satisfaction.

Types of Housing Loans Offered

To meet the varied demands of borrowers, UOB offers a range of housing loan Malaysia options:

- Fixed Rate Home Loan: Borrowers benefit from a set housing loan interest rate for the duration of their loan with the UOB set Rate Home Loan. This ensures consistency and predictability in monthly repayments, enabling borrowers to plan their budgets confidently.

- Flexi Mortgage: With UOB’s Flexi Mortgage, borrowers can manage their mortgages efficiently. It enables additional repayments to lower the loan principal and cut interest payments. These extra funds are also available for withdrawal by borrowers, giving them greater financial freedom.

Interest Rates & Payment Terms

Interest Rates:

- UOB Home Loan offers competitive housing loan interest rates for its housing loans. The housing loan interest rate may vary depending on the loan amount, financing tenure, and the borrower’s creditworthiness.

- As an example, let’s consider a housing loan with a loan amount of RM500,000 and a financing tenure of 25 years.

- The housing loan interest rate for this housing loan maybe 4.25% per annum.

Payment Terms:

- UOB Home Loan provides flexible repayment options to suit borrowers’ financial needs. In this example, let’s assume a financing tenure of 25 years.

- Based on the loan amount of RM500,000 and an interest rate of 4.25% per annum, the monthly installment for this loan can be calculated using a house loan calculator.

- The monthly installment for this loan may amount to approximately RM2,612.

Early Settlement and Partial Prepayment:

UOB Home Loan may offer options for early settlement or partial prepayment of the housing loan.

Borrowers have the flexibility to make additional payments towards the principal amount, which can help reduce the outstanding housing loan balance and potentially save on overall interest costs.

Early settlement and partial prepayment options allow borrowers to pay off their housing loan faster and potentially save on interest charges.

Customer Service Evaluation

UOB is dedicated to providing top-notch customer service and making the borrowing process as simple as possible. The skilled and committed staff of the bank offers individualised support and direction throughout the application procedure for a home loan. They can easily respond to any queries or worries expressed by potential borrowers, enabling a quick and easy loan approval process.

UOB provides various customer service options, including online platforms, phone helplines, and assistance in local branches. Through these channels, borrowers can get the information they need, follow the progress of their loan applications, and get quick assistance when needed.

UOB stands as a leading provider of housing loans in Malaysia thanks to its customer-centric philosophy and a strong emphasis on service quality.

9. Hong Leong Home Loan

Hong Leong Bank is a significant player in Malaysia’s banking sector, providing various financial services and products, including mortgage loans. Hong Leong Bank offers complete home loan solutions that are individualised to fit the unique demands of Malaysian clients.

Types of Housing Loans Offered

To accommodate various financial circumstances, Hong Leong Bank provides a range of house loan options:

- Conventional Term Loan: Conventional term loans from Hong Leong Bank have fixed repayment installments over a predetermined time. Borrowers may efficiently organise their budgets because of the regular and predictable loan instalments.

- Flexi Mortgage: Hong Leong Bank offers traditional term loans with fixed repayment payments spread out over a predetermined period of time. Borrowers can plan their budgets effectively due to the loan’s regularity and predictability of instalments.

Interest Rates & Payment Terms

Interest Rates:

- Hong Leong Bank offers competitive housing loan interest rates for its housing loans. The housing loan interest rate may vary depending on the loan amount, financing tenure, and the borrower’s creditworthiness.

- As an example, let’s consider a housing loan with a loan amount of RM500,000 and a financing tenure of 25 years.

- The housing loan interest rate for this loan may be 4.35% per annum.

Payment Terms:

- Hong Leong Home Loan provides flexible repayment options for borrowers’ financial needs. In this example, let’s assume a financing tenure of 25 years.

- Based on the loan amount of RM500,000 and an interest rate of 4.35% per annum, the monthly installment for this housing loan can be calculated using a house loan calculator.

- The monthly installment for this housing loan may amount to approximately RM2,622.

Early Settlement and Partial Prepayment:

- Hong Leong Home Loan may offer options for early settlement or partial prepayment of the housing loan.

- Borrowers have the flexibility to make additional payments towards the principal amount, which can help reduce the outstanding housing loan balance and potentially save on overall interest costs.

- Early settlement and partial prepayment options allow borrowers to pay off their housing loan faster and potentially save on interest charges.

Customer Service Evaluation

Offering top-notch customer service is a priority for Hong Leong Bank. The committed team of professionals at the bank offers individualised support and direction throughout the application procedure for a home loan. They work hard to ensure borrowers have an easy and hassle-free experience, swiftly responding to any worries or questions.

Additionally, Hong Leong Bank provides accessible customer service through in-person assistance, toll-free hotlines, and online resources. Through these channels, borrowers can access information, follow the progress of their loan applications, and get prompt assistance when required.

Hong Leong Bank has been recognised as a reliable source of house loans in Malaysia thanks to its customer-centric philosophy and dedication to service quality.

Best Housing Loans for First-time Buyers

In Malaysia, selecting the right house loan is essential for first-time buyers. Here are some of the top mortgage products designed with first-time buyers in mind:

- Maybank First Home Scheme: First-time buyers can apply for a special housing loan Malaysia programme Maybank offers. First-time buyers can realise their dream of homeownership with the support of Maybank, which offers several advantages, including reasonable housing loan interest rates and flexible financing alternatives.

- CIMB Skim Rumah Pertamaku: The Skim Rumah Pertamaku (My First Home Scheme) programme from CIMB Bank offers first-time homebuyers appealing financing alternatives and other advantages. This programme offers reduced interest rates and greater funding margins to increase first-time homebuyers’ access to housing affordability.

- RHB Easy Homeownership Campaign: The Easy Homeownership Campaign from RHB Bank is intended to help first-time homebuyers get into their ideal homes. To help first-time buyers lessen the financial burden of house ownership, this programme offers competitive housing loan interest rates, flexible financing alternatives, and special incentives.

Best Housing Loans for Investment Properties

Choosing the appropriate housing loan in Malaysia is crucial for people interested in investing in real estate. The following are some of Malaysia’s top home loan choices for investment properties:

- UOB Property Loan: A property loan designed for investment purposes is available from UOB Bank. This loan is a popular alternative for investors wishing to increase the size of their real estate portfolio since it offers competitive housing loan interest rates and flexible repayment options.

- Alliance Bank My Home Investment Loan: Alliance Bank offers a specific housing loan Malaysia for investment properties. This loan accommodates the particular requirements of real estate investors and has attractive housing loan interest rates and specialised financing options.

- Hong Leong Bank Flexi Property Financing: Hong Leong Bank provides a flexible financing option for investment properties. Investors can benefit from this loan’s reasonable housing loan interest rates, practical payback terms, and flexibility to deduct additional loan installments.

Best Housing Loans for Refinancing

Borrowers may benefit financially or reduce their interest costs by refinancing their mortgage. The following are some of Malaysia’s top refinancing options for housing loans Malaysia:

- Public Bank Flexi Home Financing-i: With the flexible home financing option provided by Public Bank, customers can cut their interest payments and loan terms. This refinancing option offers competitive housing loan interest rates, as well as the freedom to make additional payments and remove surplus funds as needed.

- RHB Smart Move Home Financing: For consumers wishing to refinance their current mortgage, RHB Bank offers Smart Move Home Financing. The convenience of online application and approval, affordable housing loan interest rates, and flexible repayment options are all features of this housing loan.

- Alliance Bank CashVantage Home Loan: The CashVantage Home Loan from Alliance Bank offers refinancing choices with competitive housing loan interest rates and the chance to access the equity in the property for cash. Borrowers who want to combine their debts or access more funds for other uses might apply for this housing loan.

Best Islamic Housing Loans

Several banks in Malaysia provide Shariah-compliant housing loans Malaysia for people looking for Islamic financing choices. Some of the top Islamic mortgages on the market are listed below:

- Bank Islam Home Financing-i: Based on the principle of Murabahah (cost plus profit), Bank Islam’s Home Financing-i offers attractive profit rates. The flexible repayment periods and financing alternatives offered by this housing loan that complies with Shariah are designed to meet the various needs of homebuyers.

- Maybank Islamic Home Financing-i: Home finance alternatives that are consistent with Shariah and Musharakah Mutanaqisah (Diminishing Partnership) are offered by Maybank Islamic. This housing loan is appropriate for Islamic financing because of its affordable profit rates and flexible repayment terms.

- RHB Islamic Bank Home Loan: Home Loan-i, a Shariah-compliant financing option that upholds the concepts of Bai Bithaman Ajil (Deferred Payment Sale), is provided by RHB Islamic Bank. Homebuyers looking for alternatives to conventional Islamic financing can use this housing loan’s competitive profit rates and flexible repayment choices.

How Do You Increase Your Chances Of Getting Approved For A Home Loan?

Applying for a house loan can be challenging for first-time homebuyers, especially if they lack trustworthy resources. A house loan eligibility question may also be on your mind.

Here are some tips on improving your chances of getting your house loan approved by the bank now that you are armed with the above fundamental knowledge regarding home loans.

1. Check your credit score

Your credit score is one of the most important variables lenders consider when approving a mortgage. Your credit score is a reflection of your creditworthiness and a prediction of your propensity to make timely debt payments. Examining and raising your credit score to maximise your chances of being approved for a home loan in Malaysia is crucial. What you can do is:

- Review Your Credit Report: Get a copy from companies that provide credit reports, such as Credit Bureau Malaysia or CTOS. Examine your report for any mistakes or inconsistencies and, if found, report them for rectification.

- Pay Your Bills on Time: Make sure to pay all your bills on time, including utility bills, credit card bills, and loan repayments. Late payments may impact your credit score.

- Reduce Your Debt: Pay off or as much down your current debts as possible. A high debt load may reflect financial difficulty and harm your credit score. Avoid taking on additional debt and concentrate on paying off existing obligations.

- Maintain a Healthy Credit Utilization Ratio: Keep your credit utilisation ratio, the percentage of your total available credit that you currently use, below 30%. A lower credit utilisation ratio indicates reliable credit management.

- Avoid Multiple Loan Applications: You should try to avoid applying for too many loans simultaneously. Multiple applications may reduce your credit score and raise questions about your creditworthiness.

You increase your reputation as a borrower and your chances of being approved for a home loan by having a strong credit score.

2. Calculate your debt-service-ratio (DSR)

Your Debt-Service-Ratio (DSR) is an additional essential consideration in the loan approval procedure. DSR is the percentage of your monthly income used to pay off obligations, such as the possible mortgage. Calculate your DSR and maintain within a favourable range to improve your loan acceptance chances. This is how:

- Determine Your Monthly Income: Determine your total monthly income, taking into account your pay, benefits, and other revenue sources.

- Calculate Your Monthly Debt Obligations: Adding together your pay, benefits, and other income streams, calculate your monthly take-home pay.

- Assess Your DSR: To calculate your DSR as a percentage, divide your monthly debt payments by your monthly income and multiply by 100. Lenders often like a DSR below 60% to ensure you have enough money to repay your loan.

Divide your monthly debt payments by your monthly income and multiply the result by 100 to get your DSR as a percentage. To ensure that you have adequate money to repay your housing loan, lenders frequently want a DSR below 60%.

3. Prove stability in your employment background

Employment stability is important to lenders since it shows a reliable source of revenue for housing loan repayments. Show proof of solid employment history to increase your chances of getting a house loan approved. What you can do is:

- Maintain Job Stability: Aim to have a stable employment history with few job alterations. Borrowers who have worked at the same company for at least two years are frequently preferred by lenders.

- Prepare Employment Documents: Obtain the pay stubs, job contracts, and offer letters required to prove your income stability.

- Show Proof of Income: Provide bank statements and income tax returns to demonstrate a consistent and sufficient income flow.

Lenders will have more faith in you if you demonstrate stability and consistency in your employment history, increasing your chances of getting a home loan.

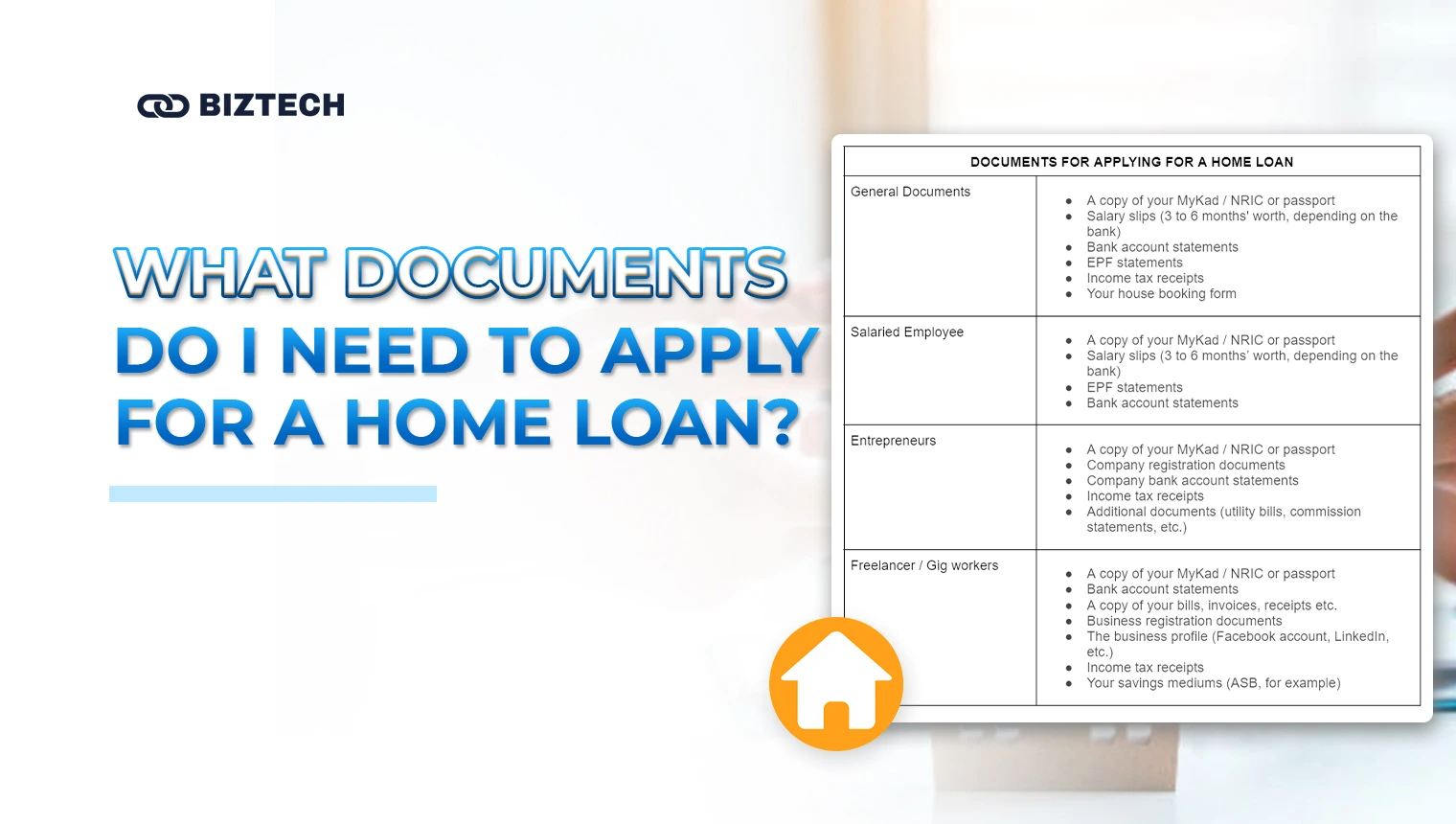

What Documents Do I Need To Apply For A Home Loan?

Are you prepared to start your online application for a mortgage? Have the following documents available for most banks to process your application so the procedure goes more smoothly.

Additionally, you can send any additional papers you may have, such as fixed deposit certificates, Amanah Saham Berhad (ASB) certificates, Tabung Haji account statements, bonds, etc. These could be helpful since they could raise your chances of approving your housing loan.

| DOCUMENTS FOR APPLYING FOR A HOME LOAN | ||

| General Documents |

|

|

| Salaried Employee |

|

|

| Entrepreneurs |

|

|

| Freelancer / Gig workers |

|

|

Summary and Conclusion

In conclusion, Malaysians must make a critical choice when selecting a house loan. In addition to Bank Negara Malaysia, CIMB Group, Public Bank Berhad, RHB Bank, Hong Leong Bank, AIA Home Loan, UOB Home Loan, Alliance Islamic Bank, Bank of China Malaysia, and many others, we have thoroughly examined the top housing loan Malaysia providers. For varied purposes, each bank offers a range of housing loans, including those for first-time buyers, investment properties, refinancing, and Islamic finance.

Malaysians should consider details like housing loan interest rates, payment schedules, customer service ratings, and the precise kinds of housing loans each bank offers to make an informed choice. To learn more, conduct in-depth research, weigh your options, and consult websites like RinggitPlus, Trusted Malaysia, and Loanstreet.

Ultimately, Malaysians should carefully consider their financial capabilities, long-term aspirations, and payback capacities before selecting a bank loan. Before making a final choice, getting professional advice and speaking with the banks directly to understand the terms and conditions is advisable. By making an informed decision, Malaysians can find low-interest housing loans for their circumstances and open the door to a smooth and successful road towards homeownership.

{kind=link}